2024 State of Accreditation Report

We are pleased to share insights from ±¨¡œ≥‘πœÕ¯ accreditation visits over the past academic year, providing ±¨¡œ≥‘πœÕ¯ members with a collective learning opportunity. In the spirit of continuous improvement, this report offers key outcomes, best practices, and future opportunities.

Have feedback? We want to hear from you!

2023–24 Accreditation Outcomes

Business Accreditation

Business Accreditation as of June 30, 2024

Accreditation Outcomes, July 1, 2023, to June 30, 2024

Notes:

Data displayed are as of June 30, 2024.

Total number of extensions: 188 (includes business and accounting).

Total number of schools achieving business accreditation: 38.

Total number of schools achieving accounting accreditation: 0.

Initial Business Accreditation

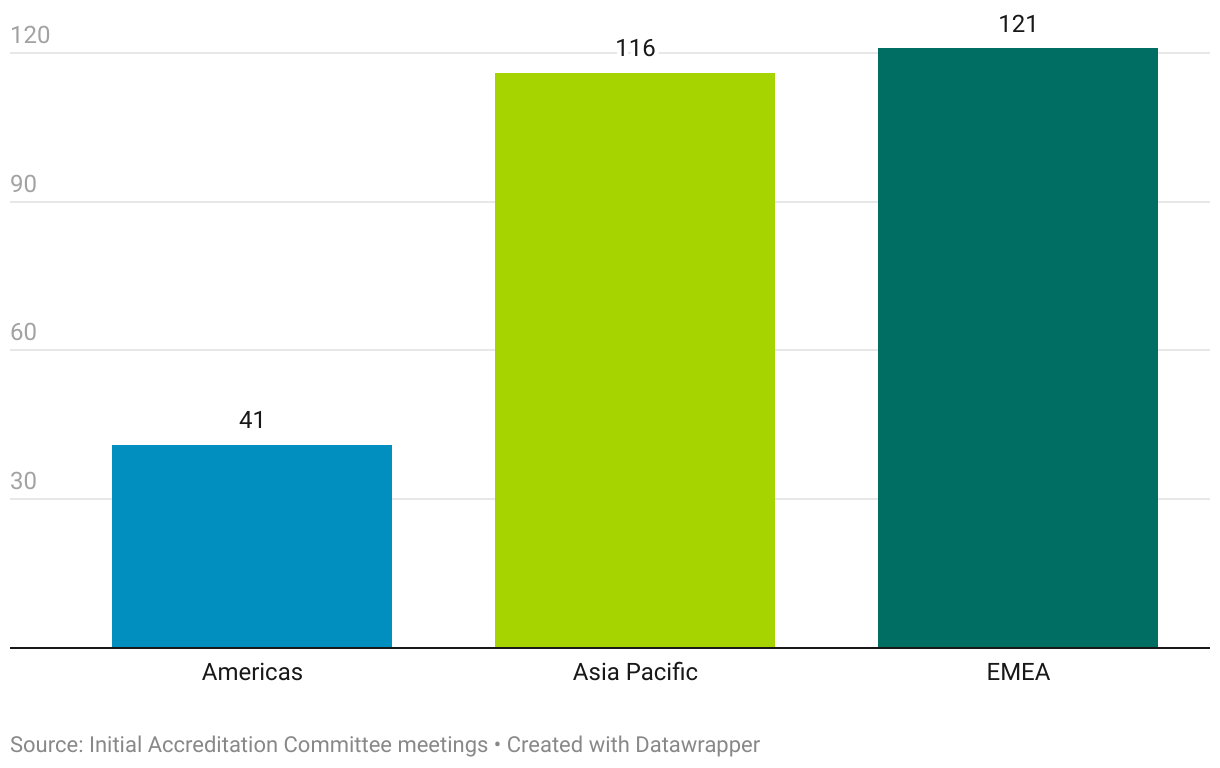

Number of Schools in Process as of June 30, 2024

| Total: 278 |

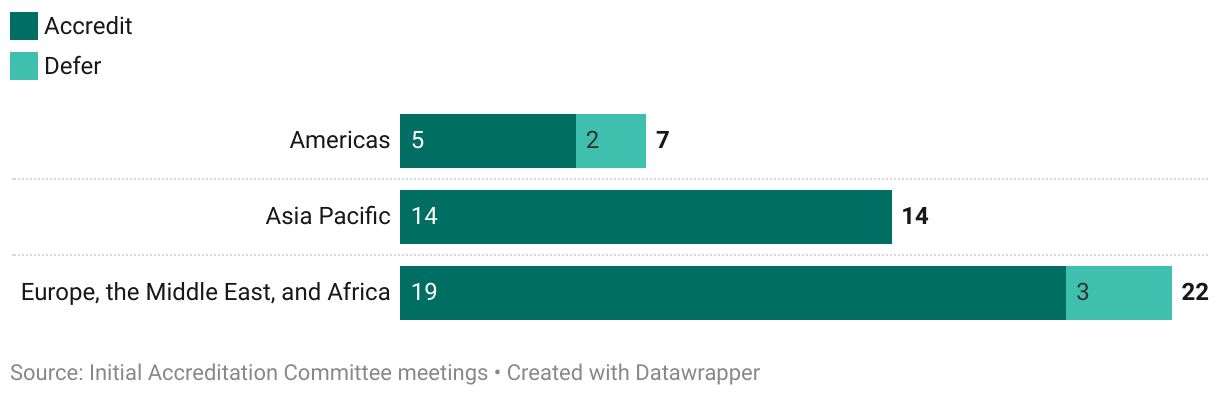

Initial Accreditation Visits, July 1, 2023, to June 30, 2024, Outcomes by Region

| Total: 43 |

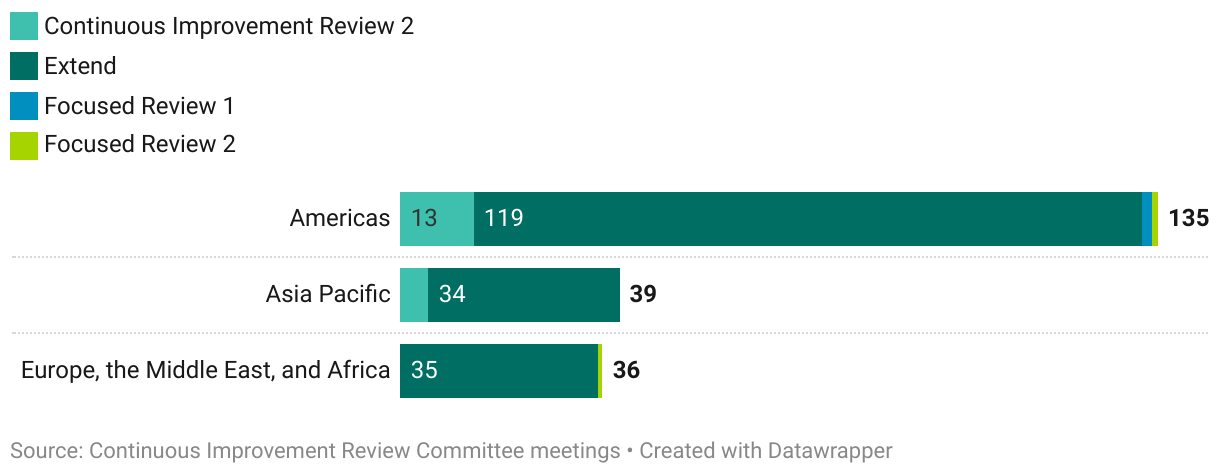

Continuous Improvement Review

Continuous Improvement Review Visits, July 1, 2023, to June 30, 2024, Outcomes by Region

| Total: 210 |

2023–24 Accreditation Insights

Business Standards Most Cited by Peer Review Teams

Schools With Visits Between July 1, 2023, and June 30, 2024, With Accredit and Extend Recommendations

In peer review team reports for both initial accreditation and continuous improvement review (CIR) visits in 2023–24, the following standards were most frequently cited as areas requiring improvement by the school’s next visit.

Standard 9 was mentioned in 94 percent of the decision reports sent, not due to peer review team findings but based on guidance from the accreditation operating committees, which emphasized the need for schools to strengthen their strategic approaches to societal impact.

Source: School decision reports.

Standard 3: Faculty and Professional Staff Resources—Common Issues |

- Faculty Qualifications and Sufficiency: Peer review teams frequently note that schools should more systematically track faculty qualifications and sufficiency ratios to monitor alignment with expected ratios. Feedback in decision reports also indicates that schools must review and refine their qualifications criteria to ensure alignment with their missions and strategic initiatives.

- Faculty Development and Support: Schools are advised to support faculty development by ensuring that faculty members have adequate time and resources to produce high-quality research and meet the school's strategic goals. In cases where administrators are held to different qualification standards than faculty, schools must have formal policies that differentiate criteria for faculty involved in significant administrative duties.

- Staffing Capacity for Strategic Growth: In light of enrollment growth and enhanced international profiles, schools are advised to invest in staffing capacity. This includes increasing the number of both faculty and professional positions to support mission-related activities and the needs of stakeholders.

For more information on insights related to Standard 3, please see Faculty Insights.

Standard 1: Strategic Planning—Common Issues |

- Strategic Plan Alignment and Implementation: Peer review teams have noted that while schools understand the need to align the strategic plan with the school mission, the strategic initiatives often lack specificity. Without specific goals and initiatives, schools face challenges with implementing, executing, and monitoring strategic plans.

- Marketing Plan and Strategy: Peer review teams highlight the importance of having a comprehensive marketing strategy to maximize program enrollment. This approach involves establishing specific enrollment targets and facilitating curriculum enhancement and faculty development.

- Societal Impact Integration: Schools are expected to intentionally incorporate societal impact into their strategic plans by selecting a focus area or areas and linking to goals that align with the school’s mission, demonstrating impact over time.

Standard 5: Assurance of Learning—Common Issues |

- Continuous AoL System Improvement: Schools are advised to continually enhance their assurance of learning (AoL) systems, ensuring that they align with the school’s mission and facilitate curriculum improvements based on assessment of learning outcomes. AoL evidence should clearly illustrate how these systems are used for ongoing improvement.

- Curricular Alignment With Learning Outcomes: Schools should demonstrate alignment between the assessment of learning outcomes and curriculum changes, focusing on program-level improvements rather than course-level adjustments, since AoL is focused on demonstration of learning outcomes at the degree program level.

- AoL Impact: Schools are advised to provide more robust evidence of how they are “closing the loop” in their AoL processes by actively using assessment data to inform and drive improvements. This involves refining the execution of AoL plans and clearly demonstrating the specific improvements that have been implemented based on assessment outcomes.

Standard 5 was cited for 78 percent of schools with a CIR2 recommendation.

Faculty Insights

Faculty Qualification Ratios for Schools With Visits in 2023–24

Note: The category of Additional Faculty, representing 4 percent, is not included above. Values have been rounded and may not equal 100 percent.

The overall participating faculty ratio for schools visited in 2023–24 is 85 percent.

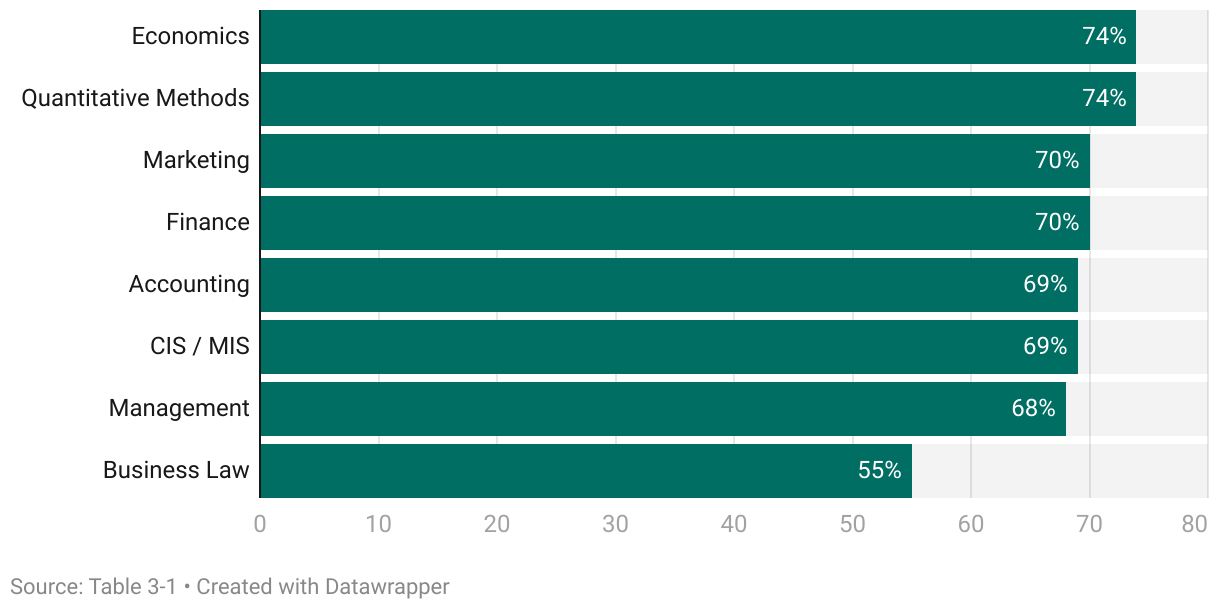

Scholarly Academic Ratios by Discipline

Most Frequently Reported Disciplines

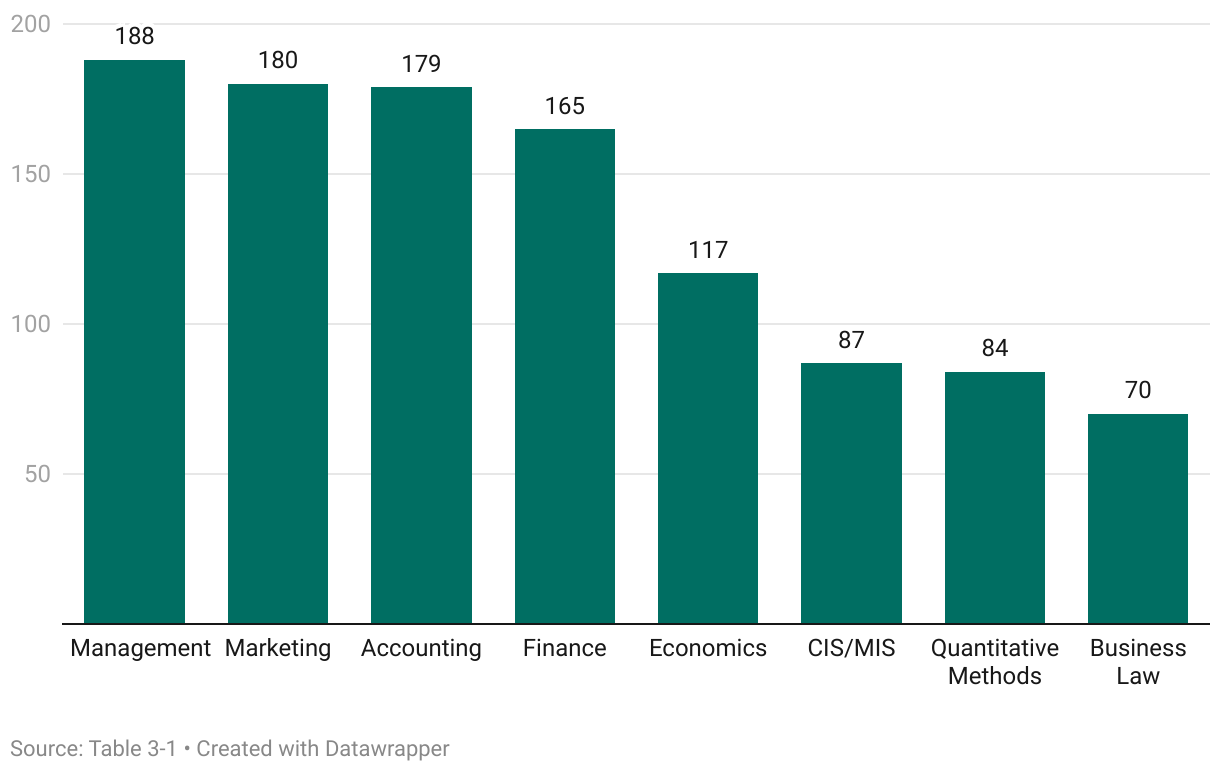

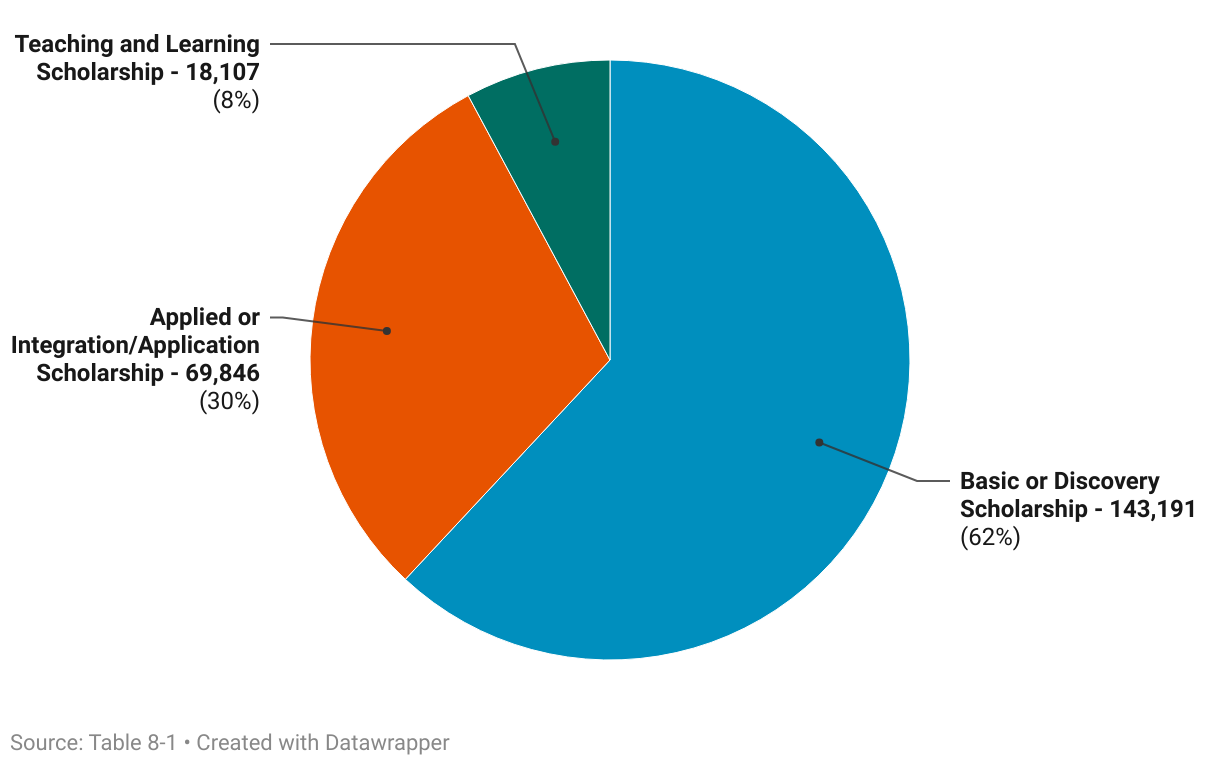

Intellectual Contributions Produced

Count of Intellectual Contributions Produced Over 5 Years by Schools Visited in 2023–24

Note: Values have been rounded and may not equal 100 percent.

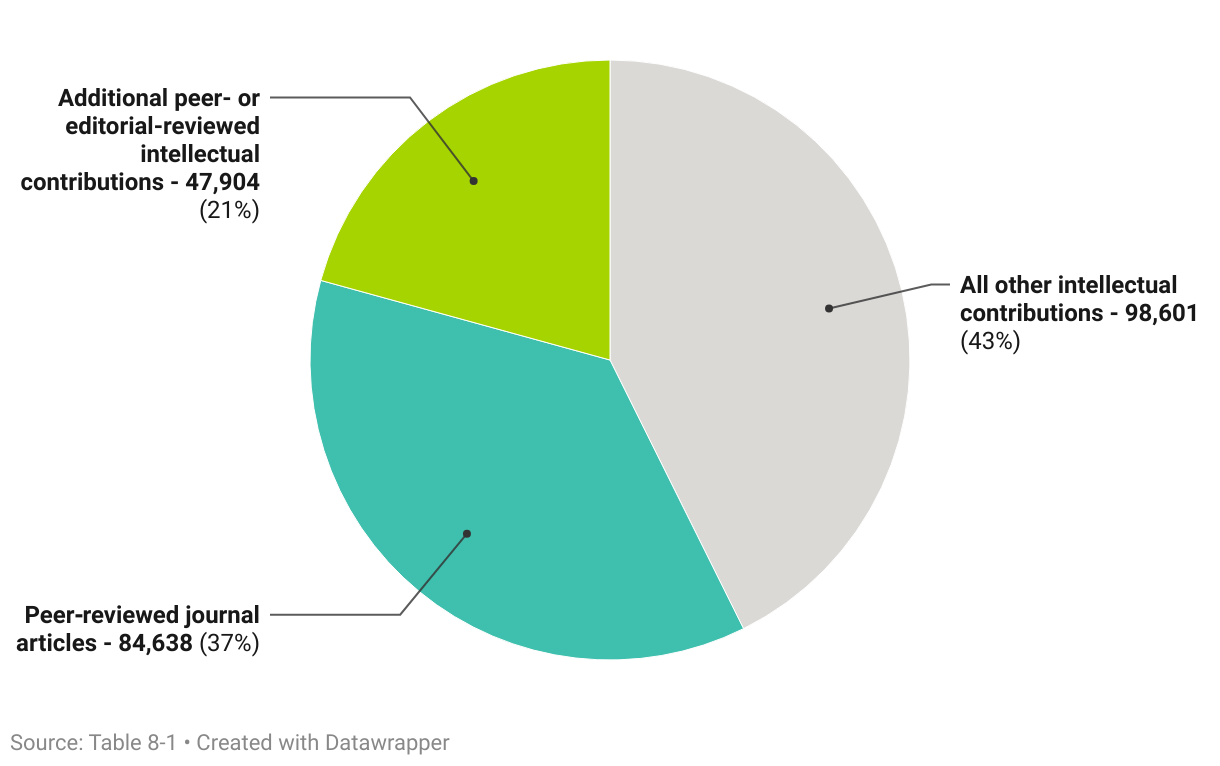

Portfolio of Intellectual Contributions

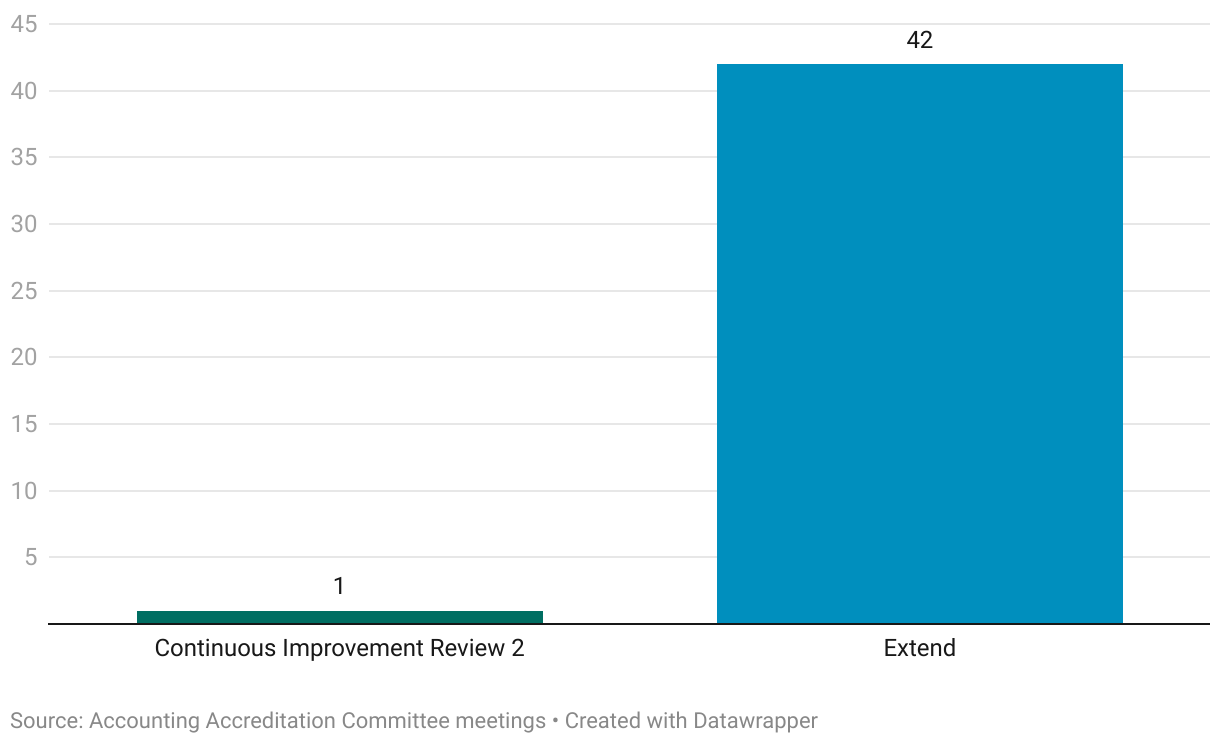

Supplemental Accounting Accreditation

Initial Accreditation and Continuous Improvement Review Accounting Visit Outcomes, July 1, 2023, to June 30, 2024

| Total: 43 |

Accounting Standards Most Cited by Peer Review Teams for Visits Between July 1, 2023, and June 30, 2024, With Extend Recommendations

Source: Accounting Unit Decision Reports

Standard A1: Accounting Academic Unit Mission, Impact, and Innovation |

- Resource Allocation: Accounting programs should ensure that their strategic plans are well-aligned with their mission and vision and clearly focused on resource allocation. The plans should also include marketing and recruitment strategies to support program growth. Accounting programs should also establish responsible parties for goals and monitor progress.

Standard A4: Accounting Curriculum Content and Assurance of Learning |

- Technology Integration in Curriculum: Accounting programs should more intentionally integrate current and emerging technologies such as generative AI into their curriculum. Peer review teams noted the importance of key stakeholder involvement to ensure appropriate technologies are employed in the curriculum.

- AoL Process Enhancement: Accounting programs should develop both direct and indirect measures to ensure that learners achieve the desired competencies. These measures may include professional exam results and alumni or employer satisfaction surveys.

- Curriculum Innovation and Alignment With Industry Standards: Accounting programs should continually innovate their curricula to align with the evolving needs of the accounting profession, including updates driven by changes in CPA exam content. Programs should also ensure that curriculum adjustments also reflect assessment outcomes, not just external industry changes.

Standard A6: Accounting Faculty Sufficiency, Credentials, Qualifications, and Deployment |

- Succession Planning for Faculty Turnover: Accounting programs should develop succession plans to address potential faculty turnover, particularly in leadership roles. Plans should include strategies for maintaining sufficient levels of Scholarly Academic faculty during periods of significant turnover.

- Faculty Deployment Strategy: Accounting programs should review their faculty deployment strategies to better align with ±¨¡œ≥‘πœÕ¯ standards while ensuring that qualified faculty are deployed across all degree programs to support high-quality learner success and achievement of learning competencies.

Volunteers

Anthony Nelson

Dean, School of Business

North Carolina Central University

Volunteer Representation for 2023–24

Notes:

This list includes individuals who served as a volunteer between July 1, 2023, and June 30, 2024, in one of the following roles:

• Operating Committee Member (Accounting Accreditation Committee—AAC; Accounting Accreditation Policy Committee—AAPC; Business Accreditation Policy Committee—BAPC; Continuous Improvement Review Committee—CIRC; Initial Accreditation Committee—IAC)

• Mentor (business or accounting)

• Team Chair (business or accounting)

• Team Member (business or accounting)

Only individuals who agreed to be listed are included. If your name does not appear and you served on one of the roles listed above between July 1, 2023, and June 30, 2024, and would like to be added, please contact us at [email protected]. Thank you.

Satisfaction With Accreditation Experience

| 94% | school satisfaction with 2020 standards visit |

| 99% | increased value of 2020 standards |

| 97% | school satisfaction with myAccreditation |

| 97% | volunteer training preparation for accreditation visit |

| 97% | satisfaction with volunteer training |

| 886 | volunteers have been trained overall on the 2020 standards |

| 132 | volunteers were trained in 2023–24 |

| 170 | volunteers completed the refresher training |

Best Practices and Innovations